In the world of investing, so much seems out of our control. Yet, there are some areas where investment outcomes are not completely at the mercy of market forces, particularly in alternative strategies such as private credit. The role of covenants and lender vigilance in direct lending highlights several levers at managers’ disposal to positively influence investment outcomes.

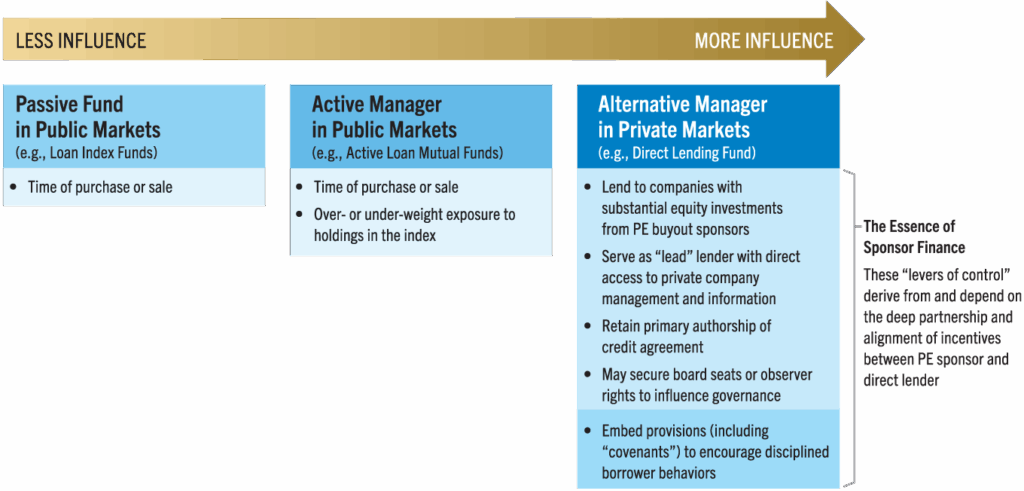

Investment strategies can be viewed on a continuum of manager control (Exhibit 1). On one end, passive investors relinquish control, seeking simply market exposure. They manage only the timing of purchase and sale. Traditional active management offers some control through selective overweighting and underweighting of index exposures, seeking to enhance returns above the market beta.

In the world of private markets, especially in private credit, managers have more levers to create value and, arguably, a greater ability to control or influence investment outcomes. They create bespoke exposures by analyzing private company information, investing alongside private equity (PE) sponsors as lead or sole lenders—often securing board seats—and by embedding explicit provisions (“covenants”) in their loan documents to monitor and/or restrict certain borrower actions.

Source: Golub Capital internal analysis

Above all these levers of control stands the essential enabling condition of sponsor finance: the relationship between the PE sponsor and the direct lending manager. Sponsors value long-term partnerships with a small group of trusted lenders, and both sides value the ability to do repeat deals. This bond is the primary mechanism for aligning incentives. In this essay, we focus on covenants as a tool for reinforcing that alignment and shaping investment outcomes.

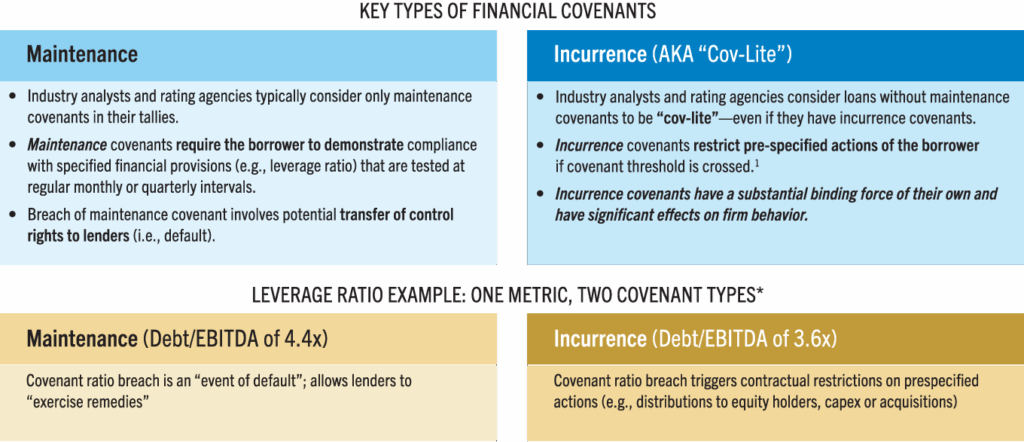

Among various loan covenant types, two that require definition upfront and are particularly relevant to this discussion are maintenance and incurrence covenants (Exhibit 2).¹ Both aim to encourage borrower discipline and preserve lender value in cases where the borrower underperforms expectations, but they function differently.

Maintenance covenants, mostly confined to private middle market loans, have two key characteristics. First, they require borrowers to report key financial metrics on a regular basis, providing lenders with early warning signals of potential distress. Second, they serve as functional levers to force engagement, where lenders can prompt corrective action if signs of stress begin to appear. The actual breach of any covenant level constitutes an event of default, giving lenders the power to accelerate the loan and/or enforce various creditor rights. Lenders may then exercise remedies, including potentially taking control of the company through stock pledge rights.

Incurrence covenants are different. They also reference a trigger point that the borrower must meet, but the level is only tested if a borrower performs certain prohibited actions. Incurrence covenants typically cover actions that increase risk to the lender, such as taking on more debt or distributing cash to equity holders without first repaying debt. If the borrower’s financial situation deteriorates, incurrence covenants provide lenders with built-in protection against the borrower making matters worse.

It is important to note that when a loan is said to be “cov-lite,” that typically means it contains only incurrence and no maintenance covenants. The term “cov-lite” often carries a pejorative connotation, which we should be alert to. Both maintenance and incurrence covenants influence borrower behavior. In a loan agreement that includes both types of covenants, the incurrence provision is typically set at a more restrictive level than the maintenance covenant.²

1. This could include the issuance of additional financing, the sale of assets or a merger.

Source: High-Yield Debt Covenants and Their Real Effects, Brauning, Ivashina and Ozdagli, August 2023.

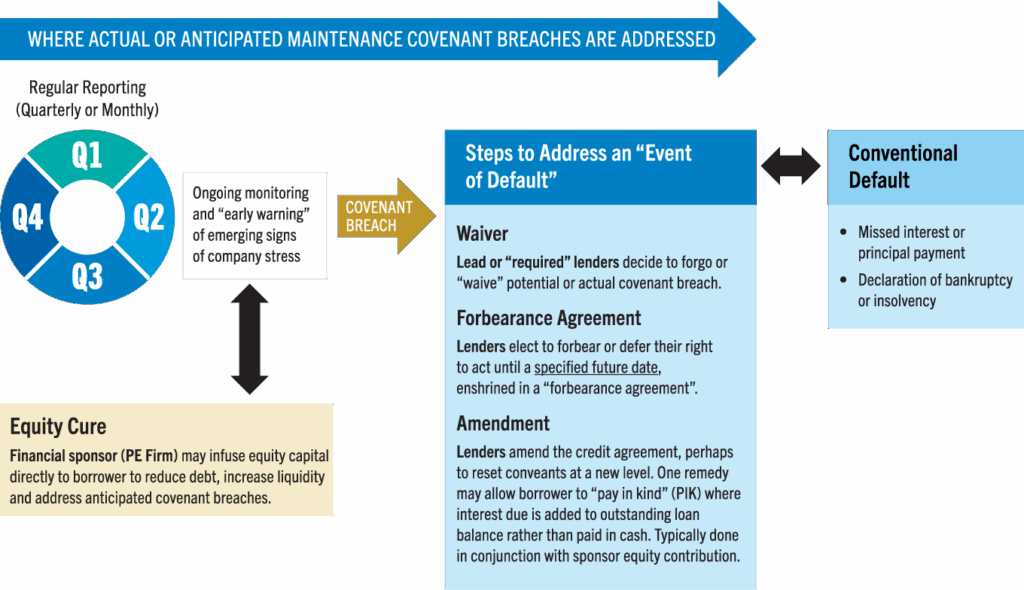

To illustrate the framework of engagement and the rough sequence of interactions associated with maintenance covenants, we depict in Exhibit 3 what we call the “zone of control.”

This schematic encompasses the ongoing monitoring and reporting that companies provide to their lenders, alongside specific covenant terms, typically based on a common leverage ratio. Lenders (and sponsors) will note any changes in the recurring reports on the company’s financial condition, including potential deterioration in the borrower’s cash or leverage levels. In some cases, the buyout sponsor may agree to infuse cash into the business to reduce borrower stress in exchange for more room on covenant tests, known as an “equity cure.”

Lender meetings can happen regularly and well in advance of any triggering action associated with a maintenance covenant based on standard loan documentation and oversight. However, once there is a breach, the firm undergoes an event of default (distinct from a conventional payment default) that sets in motion a dedicated lender–borrower meeting.

At this point, several paths may be considered. If the breach is modest and both parties expect a return to normal levels, the lender can simply waive the breach and take further action, such as enhanced reporting or board visibility. If there is concern that the stress may persist but both groups see a return to better conditions in the near future, a forbearance agreement may be reached, specifying a timeframe during which the lender agrees not to exercise remedies. If both parties agree that the covenant level is too restrictive, they can amend the agreement to reflect a different level. All of these actions—waivers, forbearance agreements and amendments—typically involve fees paid by the borrower to the lender.

Finally, if after these measures are taken, the borrower continues to struggle to meet its interest or principal requirements, the lender may seek to exercise remedies. This could include a host of actions short of taking control. However, the most extreme step in the process is installing a new board at the company—essentially taking the keys. This last step may, in some cases, prompt equity owners to consider bankruptcy for the borrower.

Source: Golub Capital internal analysis. Waivers, agreements and amendments may and typically are associated with lender fees.

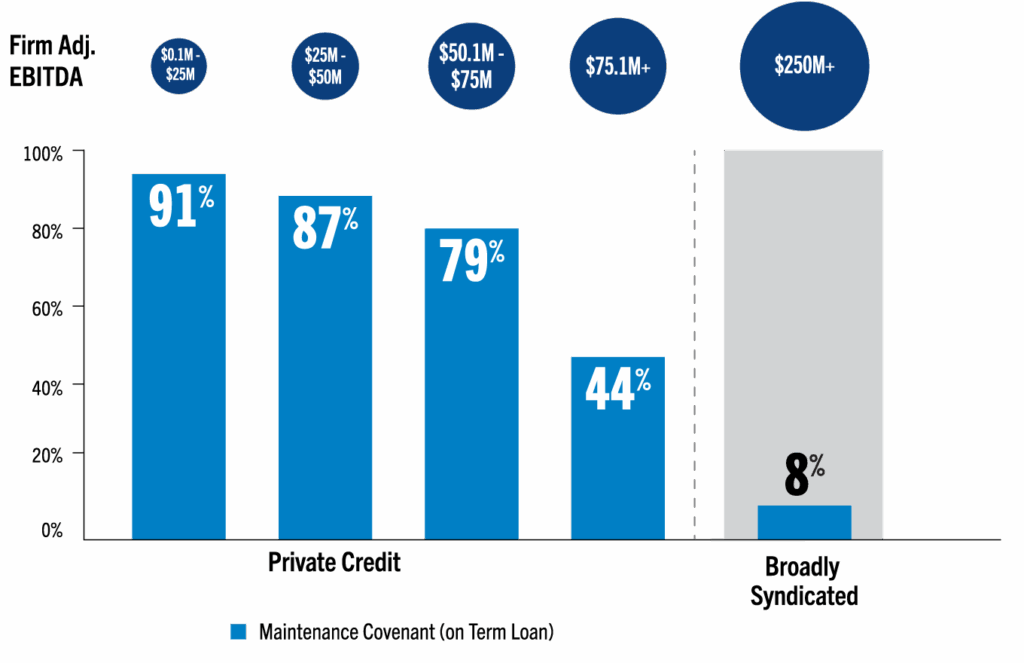

The role that maintenance covenants play in middle market direct lending is important to acknowledge. As shown in Exhibit 4, most private middle market loans include them—up to a point.

Maintenance covenants are more prevalent in smaller deals involving less mature companies, where arguably more oversight is warranted: Generally speaking, borrowers with EBITDA of less than $50 million are typically subject to a maintenance requirement. As companies grow in size and become more seasoned and resilient, the prevalence of borrowers with maintenance covenants declines. In the public broadly syndicated loan market, maintenance covenants are used only sparingly.3 While there is a reasonable argument for the diminution of maintenance covenants as company EBITDA grows, other control mechanisms remain, such as negative covenants and incurrence covenants.

1. Credit Insights Covenant Review, based on the last 12 months as of December 2024.

2. “High-Yield Debt Covenants and their Real Effects.” Brauning, Ivashina and Ozdagil, August 2023

While maintenance covenants provide value, their presence alone is no panacea. A robust credit agreement should include an array of protective documentation, extending well beyond the inclusion of maintenance covenants (Exhibit 5).

For example, if a maintenance covenant is set at a lenient level that allows substantial underperformance before it is reached, it can be as ineffective as having no covenant at all. Similarly, if the measurement of EBITDA is not clearly defined, the effectiveness of a covenant based on it can be undermined. To ensure sound credit lending practices, various add-backs that might distort EBITDA must be carefully assessed and, in some cases, restricted. The same scrutiny must be applied to borrower collateral—lenders must seek to limit leakage or the ability of the borrower to move key company assets outside the control of the creditor group.

These, and a host of other negative covenants, need to be employed to guard against borrower misbehavior. Such covenants would limit borrowers from taking on additional debt, paying equity shareholders or engaging in acquisitions or capital expenditures that might misalign their incentives with those of their creditors.

The loan document and its covenant-type provisions provide lenders with a means to guide borrower behaviors and encourage the constructive resolution of issues when they arise. They are functional levers of control, allowing private credit managers to influence investment outcomes—a rare commodity in today’s investing environment.

Maintenance covenants may be “loose,” with substantial cushion, or set at a level where substantial underperformance would have to occur before the covenant is breached. The industry sometimes calls this “covenant-loose.”

Embedding a clear definition and precise measurement of EBITDA is critical, as it drives most of the monitoring and triggering structures in an indenture agreement, including compliance with various provisions.

EBITDA can be manipulated by “add-backs” that distort earnings via actions such as immediately taking projected or pro-forma cost savings that have not yet been actioned. They are often related to acquisitions or other proposals.

Besides EBITDA, lenders seek extensive documentation to mitigate collateral leakage, provisions may limit the borrower’s ability to move key company assets (including material IP) to unrestricted subsidiaries outside of the creditor group.

A host of “negative” covenants could be employed to prevent borrowers from issuing additional debt, using cash to pay shareholder dividends, engaging in acquisitions or capex and taking any other actions that re-align incentives away from creditors.

Source: Golub Capital internal analysis

1. We should mention, in addition, a hybrid provision known as a springing covenant, which is distinct from traditional maintenance and incurrence covenants in that it applies only to the revolver, not the term loan. When a springing covenant level is triggered (or is “sprung” by reaching a certain utilization rate on the revolver, typically at ~35% drawdown level), it then requires quarterly testing, similar to a maintenance covenant. These become more common in loans to firms with higher earnings before interest, taxes, depreciation and amortization (EBITDA).

2. Generally speaking, the most common covenant metric today is a leverage ratio (i.e., debt divided by an agreed-upon definition of EBITDA). The leverage ratio is commonly used because it serves as a shorthand for the amount of debt relative to the annual cash earnings power of the business (EBITDA). Direct lenders lend against the cash earnings power of the business, and the enterprise value of the business is based on that same cash earnings power. See High-Yield Debt Covenants and Their Real Effects, Brauning, Ivashina and Ozdagli, August 2023.

3. As company EBITDA grows and the percentage of loans with maintenance covenants declines, we tend to see a corresponding rise in the number of springing covenants on the revolvers in larger deals, almost as a kind of counterbalance to the decline in term loan maintenance covenants in these deals.

In this document, the terms “Golub Capital” and “Firm” (and, in responses to questions that ask about the management company, general partner or variants thereof, the terms “Management Company” and “General Partner”) refer, collectively, to the activities and operations of Golub Capital LLC, GC Advisors LLC (“GC Advisors”), GC OPAL Advisors LLC (“GC OPAL Advisors”) and their respective affiliates or associated investment funds. A number of investment advisers, such as GC Investment Management LLC (“GC Investment Management”), Golub Capital Liquid Credit Advisors, LLC (Management Series) and OPAL BSL LLC (Management Series) (collectively, the “Relying Advisers”) are registered in reliance upon GC OPAL Advisors’ registration. The terms “Investment Manager” or the “Advisers” may refer to GC Advisors, GC OPAL Advisors (collectively the “Registered Advisers”) or any of the Relying Advisers. For additional information about the Registered Advisers and the Relying Advisers, please refer to each of the Registered Advisers’ Form ADV Part 1 and 2A on file with the SEC. Certain references to Golub Capital relating to its investment management business may include activities other than the activities of the Advisers or may include the activities of other Golub Capital affiliates in addition to the activities of the Advisers. This document may summarize certain terms of a potential investment for informational purposes only. In the case of conflict between this document and the organizational documents of any investment, the organizational documents shall govern.

Information is current as of the stated date and may change materially in the future. Golub Capital undertakes no duty to update any information herein. Golub Capital makes no representation or warranty, express or implied, as to the accuracy or completeness of the information herein.

Views expressed represent Golub Capital’s current internal viewpoints and are based on Golub Capital’s views of the current market environment, which is subject to change. Certain information contained in these materials discusses general market activity, industry or sector trends or other broad-based economic, market or political conditions and should not be construed as investment advice. There can be no assurance that any of the views or trends described herein will continue or will not reverse. Forecasts, estimates and certain information contained herein are based upon proprietary and other research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve. Past events and trends do not imply, predict or guarantee, and are not necessarily indicative of, future events or results. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss.

This presentation has been distributed for informational purposes only, and does not constitute investment advice or the offer to sell or a solicitation to buy any security. This presentation incorporates information provided by third-party sources that are believed to be reliable, but the information has not been verified independently by Golub Capital. Golub Capital makes no warranty or representation as to the accuracy or completeness of such third-party information. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Past performance does not guarantee future results.

All information about the Firm contained in this document is presented as of January 2026, unless otherwise specified.

The Morningstar Indexes are the exclusive property of Morningstar, Inc. Morningstar, Inc., its affiliates and subsidiaries, its direct and indirect information providers and any other third party involved in, or related to, compiling, computing or creating any Morningstar Index (collectively, “Morningstar Parties”) do not guarantee the accuracy, completeness and/or timeliness of the Morningstar Indexes or any data included therein and shall have no liability for any errors, omissions, or interruptions therein. None of the Morningstar Parties make any representation or warranty, express or implied, as to the results to be obtained from the use of the Morningstar Indexes or any data included therein.

“Cliffwater,” “Cliffwater Direct Lending Index,” and “CDLI” are trademarks of Cliffwater LLC. The Cliffwater Direct Lending Indexes (the “Cliffwater Indexes”) and all information on the performance or characteristics thereof (“Cliffwater Index Data”) are owned exclusively by Cliffwater LLC, and are referenced herein under license. Neither Cliffwater nor any of its affiliates sponsor or endorse, or are affiliated with or otherwise connected to, Golub Capital, or any of its products or services. All Cliffwater Index Data is provided for informational purposes only, on an “as available” basis, without any warranty of any kind, whether express or implied. Cliffwater and its affiliates do not accept any liability whatsoever for any errors or omissions in the Cliffwater Indexes or Cliffwater Index Data, or arising from any use of the Cliffwater Indexes or Cliffwater Index Data, and no third party may rely on any Cliffwater Indexes or Cliffwater Index Data referenced in this report. No further distribution of Cliffwater Index Data is permitted without the express written consent of Cliffwater. Any reference to or use of the Cliffwater Index or Cliffwater Index Data is subject to the further notices and disclaimers set forth from time to time on Cliffwater’s website.

"*" indicates required fields